Essential Guide to Double-Entry Bookkeeping for Canadian Small Businesses

Managing finances might not be the most glamorous part of running a small business in Canada, but it’s one of the most important. Whether you’re a startup in Toronto or a family-run operation in rural Alberta, getting your books right helps you avoid tax trouble, plan smarter, and sleep better at night.

That’s where double entry bookkeeping comes in. At One Accounting, we help Canadian small businesses like yours set up streamlined bookkeeping systems that bring clarity, accuracy, and peace of mind.

In this guide, we’ll walk you through everything you need to know about double entry bookkeeping from the basics to best practices tailored specifically for Canada’s unique business landscape.

Let’s start with the basics, what exactly is double entry bookkeeping and why should Canadian small business owners care?

Understanding Double-Entry Bookkeeping

Getting a grip on how your money moves is essential for running a successful business in Canada. Double entry bookkeeping gives you a method to record transactions in a balanced, structured way. When done right, it brings clarity to even the most complex financial activities.

Double entry bookkeeping means every financial transaction is recorded twice, once as a debit and once as a credit. This system keeps your financial records balanced and complete.

The main reasons this system is ideal for Canadian businesses are as follows:

- It ensures all your books follow the Assets = Liabilities + Equity equation.

- It provides a full view of your company’s financial position.

- It helps you stay compliant with Canada’s tax laws and CRA regulations.

Now that you understand the concept, let’s dive into the parts that make the system function smoothly.

Core Components of the System

Before you start recording transactions, it helps to understand the building blocks of your accounting system. These core elements are the heart of double entry bookkeeping. Knowing how they work will make the entire process more efficient for your Canadian business.

To run double entry bookkeeping smoothly, you’ll need to use the components listed below:

- Accounts: These include assets, liabilities, equity, income, and expenses. Each account tracks a specific type of financial activity.

- Journal Entries: Every transaction is recorded in the journal with both debit and credit entries. This is your first record of financial events.

- General Ledger: This is the master file where all journal entries get posted. It serves as a central hub for your business’s finances.

- Trial Balance: A quick check to make sure all debits and credits match. It helps you spot errors before finalizing reports.

Setting Up Double-Entry Bookkeeping in Canada

Getting started is often the hardest part. But with a clear setup, even first-time business owners in Canada can confidently manage their books. Setting it up right ensures your system works smoothly from day one.

Here’s how to build your bookkeeping process from the ground up in Canada, as follows:

- Create a Chart of Accounts: Tailor it to your business activities and industry. A proper chart helps organize your financial data effectively.

- Pick a Software That Works in Canada: Options like QuickBooks Online, Xero, or FreshBooks all support double entry bookkeeping and include Canadian tax features like GST/HST. These tools make compliance easier and save time.

- Set Up GST/HST Tracking: If your business is registered for GST or HST, your bookkeeping system must reflect these taxes correctly. Mistakes here could lead to issues with the CRA.

One Accounting can help you set everything up the right way from the start, so you stay compliant and efficient.

Let’s walk through how to use double entry bookkeeping for your day-to-day business activities.

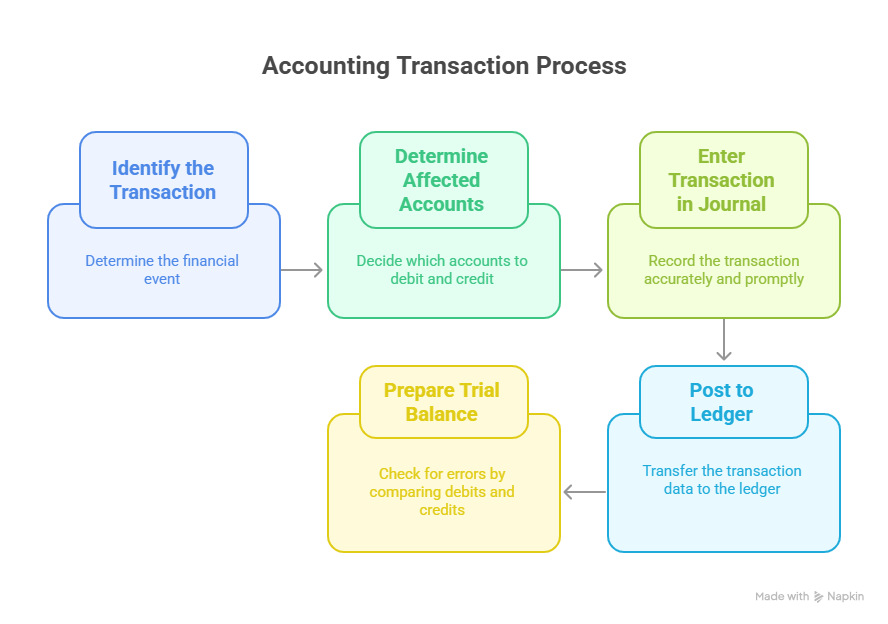

Recording Transactions: Step-by-Step

Recording your transactions is where the real work happens. With double entry bookkeeping, accuracy is everything. Each entry must reflect real financial activity, especially with Canada’s strict tax rules.

- Identify the Transaction: What happened financially? Was something purchased, sold, or paid?

- Determine the Affected Accounts: Which account should be debited? Which one is credited? Knowing this ensures the books stay balanced.

- Enter the Transaction in Your Journal: Be accurate and timely. Missing details can throw everything off.

- Post to the Ledger: Transfer the data from the journal to your ledger. This keeps all transactions in one central record.

- Prepare a Trial Balance: Regular checks help catch errors early. If the numbers don’t match, something goes wrong.

With this step-by-step process, your Canada-based business will always have reliable records at your fingertips.

Benefits of Double-Entry Bookkeeping

The time you invest in bookkeeping pays off in many ways. With the right setup, you can make confident financial decisions and avoid costly mistakes. For small businesses in Canada, these benefits are too valuable to ignore.

- Accuracy: Every transaction is double-checked automatically. This minimizes the risk of errors or missing entries.

- Better Financial Insight: Know exactly where your money is going. Accurate records help you create realistic budgets and forecasts.

- CRA Compliance: Stay on the right side of Canadian tax laws. You’ll be ready for audits or filings without the last-minute scramble.

- Fraud Prevention: Spot suspicious activity faster. A balanced system makes it easier to identify red flags.

This approach makes your books more trustworthy, something every Canadian business owner needs.

Common Mistakes and How to Avoid Them

Mistakes in bookkeeping are common, especially when you’re managing multiple roles. But with awareness and the right habits, they’re easy to avoid. Learning from others’ errors can save your Canada-based business a lot of trouble.

- ❌ Missing Transactions: Always record your expenses and income on time. Waiting too long can lead to confusion and incorrect reports.

- ❌ Wrong Account Categories: Take time to understand your accounts or get help from a pro. Misclassification can affect your taxes and decision-making.

- ❌ Not Reconciling Bank Statements: Compare your records with actual bank data regularly. Reconciliation helps catch discrepancies early.

From bank integrations to real-time access, here’s how technology makes everything faster and more accurate.

Leveraging Technology for Efficiency

Modern accounting tools can save you time and reduce stress. If you’re running a small business in Canada, automation can be a game changer. Instead of wrestling with spreadsheets, let technology handle the heavy lifting.

- Automate Tasks: Let software handle recurring invoices, payments, and reports. This means less manual entry and fewer errors.

- Integration with Banks: Link your Canadian bank account directly to your software. Transactions will sync automatically.

- Cloud Access: Manage your finances from anywhere in Canada, at any time. This makes remote work and team collaboration easier.

One Accounting helps you choose and customize the right tech stack to make bookkeeping feel effortless.

Conclusion

Double entry bookkeeping isn’t just an accounting method, it’s a smart business move. For Canadian small businesses, this system is key to staying organized, tax-ready, and financially confident.

- Make better decisions,

- Catch errors before they become problems,

- And build a business that thrives long-term in Canada.

At One Accounting, we specialize in setting up and managing double entry bookkeeping systems for small businesses across Canada. From software selection to full-service bookkeeping and tax prep, we offer customized solutions that save you time and give you peace of mind.

Want to take control of your finances without the stress? Let One Accounting help you get started with double entry bookkeeping today.