How Experts Handle Debit vs Credit Bookkeeping to Keep Your Books Balanced

Managing your finances as a business owner can feel overwhelming, but it doesn’t have to be. With the right support, you can turn complicated accounting systems into tools that support your success. That’s where One Accounting comes in.

Our expert team utilises proven methods and advanced software to handle every aspect of your books, particularly one critical system: debit versus credit bookkeeping. This foundational practice keeps your finances clean, accurate, and balanced.

In this article, we’ll walk you through how professionals handle debit vs credit bookkeeping from start to finish, so you can understand how we keep your business running smoothly behind the scenes.

Grasping the Basics: What “Debit vs Credit Bookkeeping” Means

To understand how experts manage your books, it’s important to start with the foundation of accounting. Many business owners hear terms like “debit” and “credit” without knowing how they actually function. But once you understand how they balance each other, everything becomes clearer.

That’s where debit vs credit bookkeeping comes in. This method ensures that every transaction is recorded in two places to maintain accurate bookkeeping. It’s the backbone of a reliable financial system used by businesses of all sizes.

Before diving deep, it’s important to understand what debit vs credit bookkeeping actually means. In double-entry accounting, every financial transaction affects at least two accounts, one with a debit and the other with a credit. This ensures that your books remain balanced.

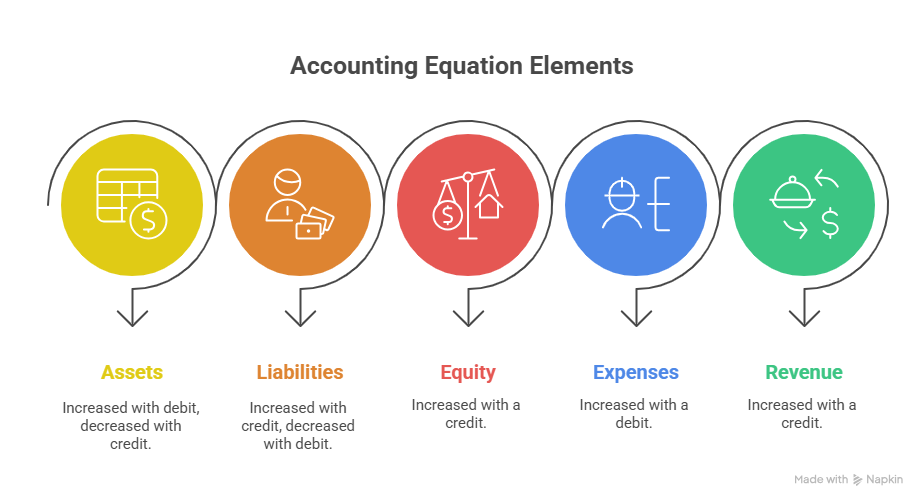

To maintain accurate books, you need to understand how different accounts respond to transactions; the behavior of each is explained in the following:

- Assets: Increased with a debit, decreased with a credit

- Liabilities: Increased with a credit, decreased with a debit

- Equity: Increased with a credit

- Expenses: Increased with a debit

- Revenue: Increased with a credit

All of this supports the fundamental accounting equation:

Assets = Liabilities + Equity.

When done right, debit vs credit bookkeeping guarantees that your books stay in balance, which helps avoid costly mistakes down the line. Even a basic understanding of these rules can help business owners have more meaningful conversations with their accountants.

Once you understand how debits and credits function, the next step is applying them correctly to real-world transactions through journal entries.

Crafting Precise Journal Entries

Once you know what debits and credits mean, you can begin applying them to real-world transactions. But doing so accurately requires experience, attention to detail, and a solid process. That’s where experts shine.

Bookkeepers trained in debit vs credit bookkeeping know exactly how to record every transaction. They break down what’s happening, which accounts are affected, and how each should be adjusted.

To maintain accuracy in bookkeeping, professionals rely on these foundational journal entry steps, detailed as follows:

- Step 1: Identify the accounts impacted

- Step 2: Determine whether they’re increasing or decreasing

- Step 3: Apply the correct debit or credit based on the account type

To illustrate the debit vs credit process, let’s look at how specific transactions are captured in the books, as shown below:

- Buying Equipment with Cash

- Debit: Equipment

- Credit: Cash

- Receiving a Customer Payment

- Debit: Cash

- Credit: Accounts Receivable

- Paying for Utilities

- Debit: Utilities Expense

- Credit: Bank

Each entry must be balanced before it’s posted. For example, if you debit $500 to an equipment account, you must credit $500 from another account. That’s the whole point of debit vs credit bookkeeping, every action has an equal and opposite reaction.

At One Accounting, we follow a checklist before recording journal entries. We verify the source documents, determine the impact, and only then make the entry. This reduces errors and ensures your books are always accurate.

With entries complete, we move into the stage where structure and visibility matter most: the general ledger and T-accounts.

Leveraging the Power of the General Ledger and T‑Accounts

Once transactions are entered, they need to be tracked over time. That’s where general ledgers and T-accounts come into play. These tools give structure to your records and make it easy to trace entries back to their source.

Professionals use T-accounts as a visual tool to separate and organize debits and credits. These tools simplify complex transactions and make it easier to catch errors early. For example, a T-account helps you quickly see if a cash account was overdrawn due to too many credit entries.

To streamline ledger management and improve accuracy, professionals use specialized bookkeeping platforms, which include the following:

- QuickBooks Online – great for small businesses and automation

- Xero – ideal for real-time collaboration and reporting

- FreshBooks – user-friendly for freelancers and service providers

These platforms help us streamline debit vs credit bookkeeping through features and automation tools such as the following:

- Auto-updating ledgers

- Flagging discrepancies

- Reducing manual errors

For growing businesses, these tools become a critical part of financial transparency. Our clients at One Accounting get monthly summaries from their general ledger to help them understand where their money is going.

Once your ledger is filled out, the next focus is ensuring that all accounts reconcile properly with your bank and vendor records.

Running Regular Trial Balances and Reconciliations

Recording entries isn’t enough, you also need to check that everything adds up. That’s why professionals run regular trial balances and reconciliations. These steps are critical for maintaining clean and trustworthy books.

A trial balance is a report that lists all ledger accounts and their balances. If the sum of all debits doesn’t match the sum of all credits, we know something’s wrong.

Each type of reconciliation targets a different area of your books. Common reconciliation categories are outlined below:

- Bank Reconciliation – Compares internal records with bank statements

- Credit Card Reconciliation – Ensures every charge is accounted for

- Supplier Statement Reconciliation – Matches supplier invoices and payments

Reconciliations help us identify and correct bookkeeping issues by catching problems such as those listed below:

- Duplicate entries

- Missing transactions

- Unapplied payments

Running these checks regularly ensures consistency in debit vs credit bookkeeping. At One Accounting, we run reconciliations monthly or even weekly for clients with higher transaction volumes. This proactive approach helps you avoid financial surprises.

No bookkeeping system is perfect, but professionals know where to look and how to fix errors when they inevitably occur.

Spotting and Correcting Errors Proactively

Errors are inevitable, but catching them fast makes all the difference. Experts are trained to look for red flags and know exactly where to look.

It’s important to recognize which types of mistakes happen most often in debit vs credit bookkeeping, such as those listed below:

- Misplaced entries – e.g., debiting instead of crediting

- Omissions – forgetting to record a transaction

- Misclassifications – using the wrong account

We detect these bookkeeping errors using a combination of review methods and tools, as follows:

- Running trial balances

- Comparing reports

- Using reconciliation tools

Once we identify the problem, we fix it by using adjusting journal entries. These entries correct the original mistake while keeping the books in balance.

In one case, we helped a client spot a $2,000 misposted payment that would have otherwise impacted their year-end taxes. That’s the power of expert review, it saves money and keeps your records honest.

Now that we’ve covered how to record, organize, and audit transactions, let’s explore the daily habits that keep everything running smoothly.

Expert Best Practices for Maintaining Balance

Experts don’t just work harder, they work smarter. We follow best practices that prevent problems before they start. This is what keeps debit vs credit bookkeeping consistent and reliable.

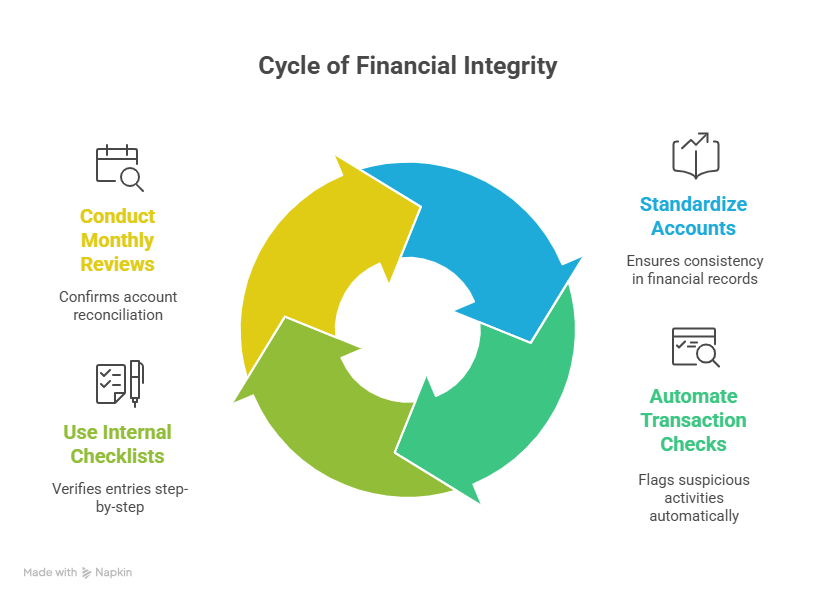

These expert strategies help us prevent errors, increase efficiency, and deliver trustworthy results for every client, as follows:

- Use of a standardized chart of accounts – ensures consistency

- Automation rules – flag suspicious transactions

- Internal checklists – verify every entry step-by-step

- Monthly reviews – confirm all accounts reconcile

We also conduct quarterly review sessions for businesses looking to grow. During these meetings, we analyze trends, review your balance sheets, and prepare you for the next stage of growth. That’s how bookkeeping becomes a strategic tool, not just a back-office task.

To elevate bookkeeping from a chore to a strategic advantage, professionals use smart software solutions that integrate seamlessly into their workflow.

Using Software and Automation to Streamline Debit vs Credit Bookkeeping

Modern bookkeeping blends expertise with technology. While human review is still essential, automation tools help handle repetitive tasks and reduce risk.

At One Accounting, we integrate technology into every step of debit vs credit bookkeeping. That means less time fixing problems and more time adding value to your business.

When integrated properly, automation features enhance efficiency and accuracy. Common capabilities include those listed below:

- Automatically post recurring transactions

- Receive alerts for unusual activity

- Create reports in real-time

- Sync bank feeds and credit card data

For example, we set up bank rules in QuickBooks to automatically categorize recurring expenses like rent and utilities. These little efficiencies add up, saving hours every month while maintaining the integrity of your books.

All this effort leads to one major benefit: empowering business owners with insights, clarity, and the confidence to make smart decisions.

Translating Balanced Books into Client Value

Why does all of this matter? Because balanced books don’t just help you avoid mistakes, they help you grow. Reliable data supports smart decisions.

When your bookkeeping is handled professionally, the benefits extend far beyond compliance, business owners consistently gain the following:

- Accurate reports – for planning, budgeting, and forecasting

- Audit readiness – no scrambling during tax season

- Financial clarity – know where your money is going

- Peace of mind – trust that your records are always right

You’ll also gain the confidence to answer tough financial questions from lenders, investors, and auditors. Your finances become an asset, not a liability, when they’re prepared with precision and care.

After exploring every layer of debit vs credit bookkeeping, it’s clear that expert guidance makes a world of difference in managing your finances.

Conclusion

Getting debit vs credit bookkeeping right is more than just good accounting, it’s good business. From journal entries to trial balances, reconciliations to error correction, it’s a process that demands experience, precision, and care.

At One Accounting, we do the heavy lifting for you. Our team of professionals keeps your books balanced, your data clean, and your decisions informed. Whether you’re running a startup or managing a growing enterprise, we help you stay financially sharp and stress-free.

So why not stop worrying about your books? Let One Accounting handle the debits and credits, so you can focus on building your business with confidence.